Thoughts on Software

Is the sky falling? Where is the bottom?

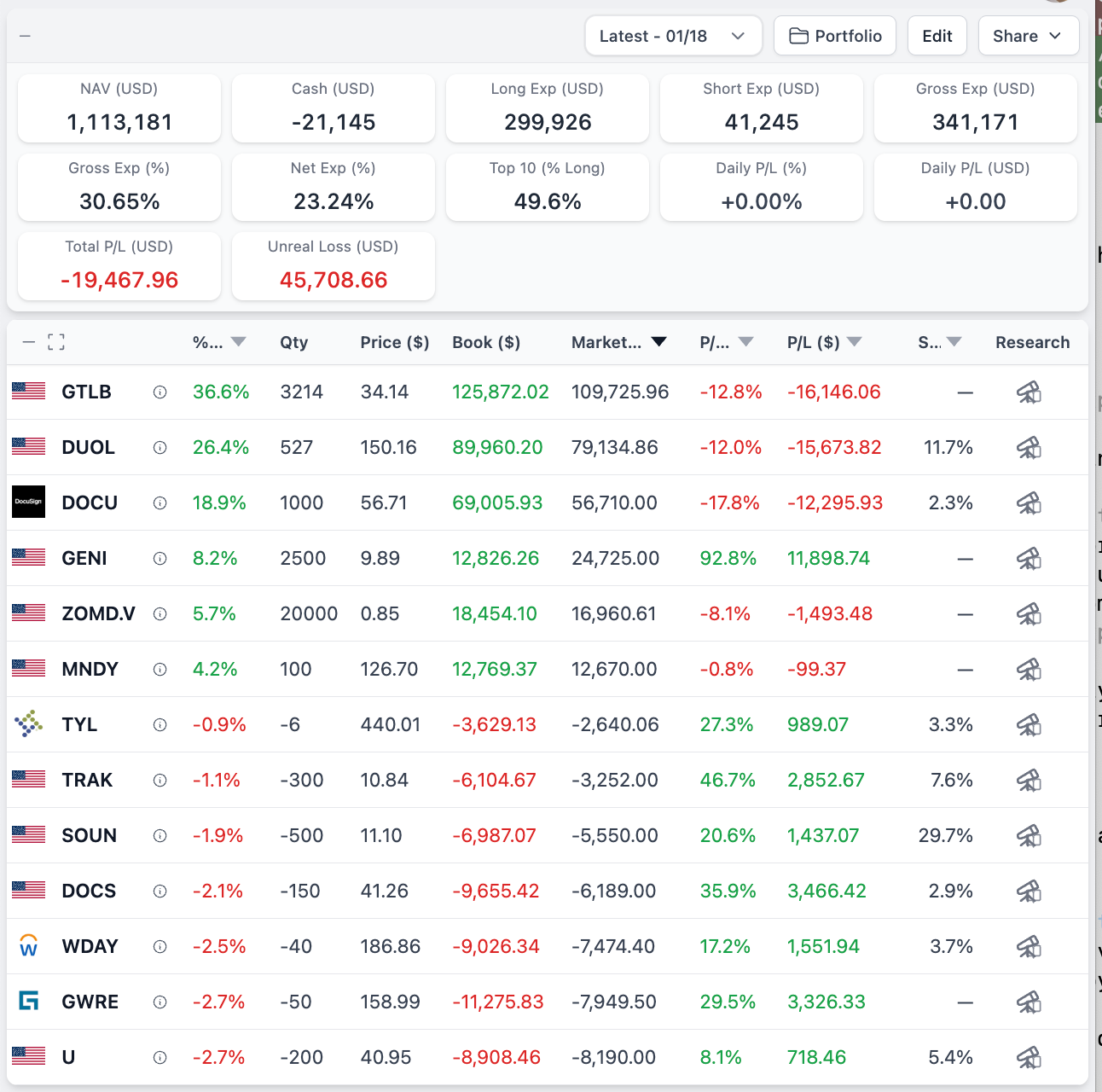

Just a quick update, unlike my more recent / comprehensive Substack posts, but wanted to get something out on the current state of the Software Ecosystem. I’ve been thinking "Ok I really need to figure exactly how much exposure I have to Software right now" over the weekend, but then realized "Oh I already built that, i just need to filter by industry in my ALPHAPORT portfolio (https://bit.ly/4jLbk0l)".

As you can see in the link if you filter by industry - application software, its 23.24% of my net exposure after the sell offs, which is a little high for someone that believes that the hyperscalers largely take all the economics out of the software ecosystem.. but I think the distribution of outcomes for the three big positions is pretty good here. Could I be wrong? Sure, we will just have to see how it goes.

Of these 3, I personally think $GTLB is the most defensible though you are still paying a higher price. People are talking about the company like the sky is falling but GTLB has half of the Fortune 500 signed up, with no customer over 5% of revenue. These are easy throw away lines, but when you look at the actual deals with major financial institutions like UBS and Goldman Sachs, or Defense Contractors like $LMT or $NOC, these guys aren't just ripping out their giant CI/CD pipelines because the CEOs son built a shovelware video game with Claude Code on a Sunday. $1200 a year is also just not that much money for their Ultimate tier. I'm using $GTLB myself and while i'm an incredibly cheap human being, $1200 a year is below my line. I am spending 5x that on AI for sure right now. And when I ran a video game studio, we used to have artists that were earning 50-80k a year, and their Autodesk license for 3dsmax or Maya was costing us 3k a year! And they used other stuff too from $ADBE, like Substance Painter etc.

I also see $GTLB as the stodgier companies way into using more AI in their workflows.

"Ok we'll pay for Gitlab Ultimate and some Claude Code tokens, now tell us how to use AI better"

"Sure, you will be amazed at how much shit this can do now"

"Great".

A couple questions for the coming week are where I would close out the Tyler and Guidewire shorts (they both still seems expensive, but they legitimately have good businesses, they were just priced for perfection). Maybe 6x-7x rev. You're still paying 13.5 billion for 1.27b of revenue with Guidewire. Mind boggling to me. You can come up with reasons that this might work out, but its hard for it to be absolutely amazing from this starting point. People will say "If you pay 13.5 billion for it now, and it grows 20% a year for 5 years, your ROI in 5 years is 20%".

Ok, but what about the year growth finally stalls. At some point it will. Maybe its in 7 years, maybe 10, but when growth goes from 20% to 10%, you will then lose 1/3 of your money. So its not as simple as just saying "10x rev is fine since they will pay 10x rev when I want to sell, since this is quality". Maybe you can perfectly time the exit the year before growth starts declining, but I certainly can't!

Companies I think are a little oversold and will still do well? $SAP, $CRM and $NOW are all unlikely to be ripped out because of some vibe coding. These services cross different verticals in the same business. A useful mental model is just to imagine telling all these teams that you are going to replace this software you all finally got working in between their various departments (in 2023 maybe?), with something George in the digital team builds over the weekend. Pretty lol if you ask me.

But for me, the starting prices are still quite high. $SAP looks particularly appealing of these 3, with what I view as a stickier product at a better price.

But you're still paying 235 billion euros for 36.5 billion of revenue. People will look at growth, or margin expansion, and make counter arguments, but to me, those things are much more fragile than sales if we have an uncertain future. Do I think people will rip out $SAP because of Claude Code? Very unlikely. Do i think that $SAP will be able to raise their prices at inflation + 4% for the foreseeable future because they have their customers completely locked in? I think that's more nebulous. Very possible, but not a certainty, and at 6.5x rev its still a little expensive for the risk. I think that one is getting quite close for me though, especially if I was rotating one of my losing software cos into it. I do also think that if there are software layoffs, for example $SAP themselves reduce headcount by 20%, the laid off engineers are going to need to get jobs somewhere - perhaps they will create competitor products because they have no choice. So we will see more software overall (more $GTLB seats), but compressed margins. This is one reason it's important not to overpay for revenue - revenue is always defensible at scale. $SAP will ALWAYS work with a 5% net income margin. Maybe even a 10% net income margin. But at 10x sales, a 10% net income margin is a PE of 100. This is why, for me, 3x sales is really where I consider most companies as valid investments (30x PE at 10% net income margin, which is a pretty normal exit margin for most businesses. Still not that cheap!).

One thing this latest sell off has made really clear to me is how many investors legitimately think buying companies at 9-10x rev is cheap, or that using EV/FCF to value a software company is not a total fugazi. In a world of relative valuation and stock screeners, I think people have outsourced their critical thinking skills to a few metrics. "Here's where the company sits on the relative valuation PEG chart, LFG". How deeply have you thought about how margins actually inflect here? What leads to good business results for any given software business? Where are the risks? On the other hand, narratives that make no sense to me spread like wildfire. If you legitimately believe 50% of software engineers are going to be out of work, you should just buy way out $QQQ puts, because we are going to be talking about a much worse situation than $MNDY rerating to what I view as a much more reasonable valuation.

Anyway, https://ALPHAPORT.AI makes it really easy to track your portfolio like this by sector, long/short weights, etc (https://bit.ly/4jLbk0l), and it's free if you use it with Interactive Brokers. Using Plaid, it also supports almost every other brokerage, although that is a paid feature ($10 a month though, a pittance!). If you want to sign up but have any trouble, feel free to DM me, i'll help you out.

In Sweden we have app Truecaller down 80% because google changed its advertisement algo and it lost like 30% income, now trading at like P/S 1.5, while insiders are buying like hell

I envision volatility as companies find out the limits of ai coding. IOW more project managers and fewer coders, but does that require hiring? Musical chairs? Timeljne estimation process adjustments. And as the ground troops and generals go back and forth on this how does it affect strategy and planning? Volatility.