May went well

Great YTD returns, some interesting new positions, and solid product innovation with ALPHAPORT.AI

Nothing in here is investing advice, it is a journal of my own investing decisions. Some of those decisions are pretty bad and will probably lose money. For example, have you seen how my short book is doing? I also might just randomly decide to sell something that I was really excited about in this post (though you can see a snapshot of my portfolio daily using the link in my X profile here: https://x.com/ALEXEIMARTOV). Anyway, talk to a trusted financial adviser, and perhaps consider ETFs.

For this year, and generally career-wise in life, I have 3 goals

Outperform SPY

Write about it in this free Substack

Build my InvestTech app ALPHAPORT.AI into a leading InvestTech platform and the first place I turn for my own portfolio tracking, investment research, etc.

May was a solid month, with the portfolio increasing from 25% YTD to 49%. With SPY up 10.73% (still a tonne!) this represents very good performance obviously.

There are a few X accounts who have done better (options + momo stocks have lead to some insane returns on some accounts), but overall I am quite satisfied.

It seems almost unbelievable that some are posting well over 100%, but if I look at my own positions, if I simply hadn’t hedged the main positions I would probably be around there (shorting $EWY against SK Hynix, $ARM against Softbank, and selling $2120 calls on Sandisk for $640 per lot). I am happy with the decision however, perhaps with the exception of Sandisk, where I may take the hedge off (more on that later). The market does feel somewhat extended here, even though I think the AI trade has further to go.

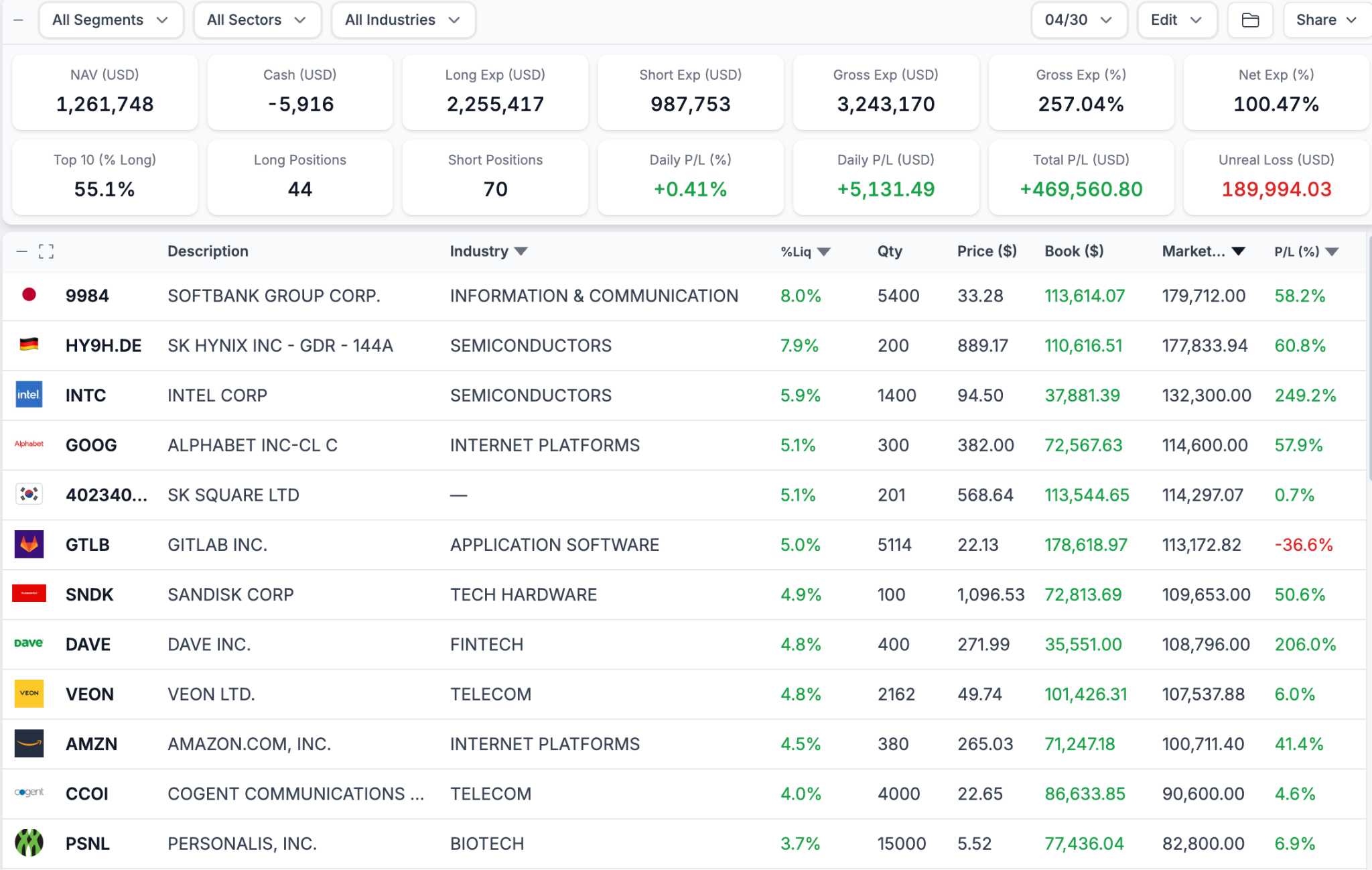

Here is where we left off:

And here is where we are today:

YTD across the two accounts is 64.42% in the larger account and 29.64% in Acn 1 (LO account), and 64.42% in Acn 2 (long short account).

Bookkeeping: Jan 1, Acn 1 started at $473,000 and Acn 2 started at $586,420

So the weighting used is roughly 45% to Acn 1 and 55% to Acn 2. Although I have made a few modest cashouts etc, this is the weighting I am using to calculate my returns as it is very close. So YTD = (.45 * 29.64%) + (.55 * 64.42%) = 48.89%.

What happened in May?

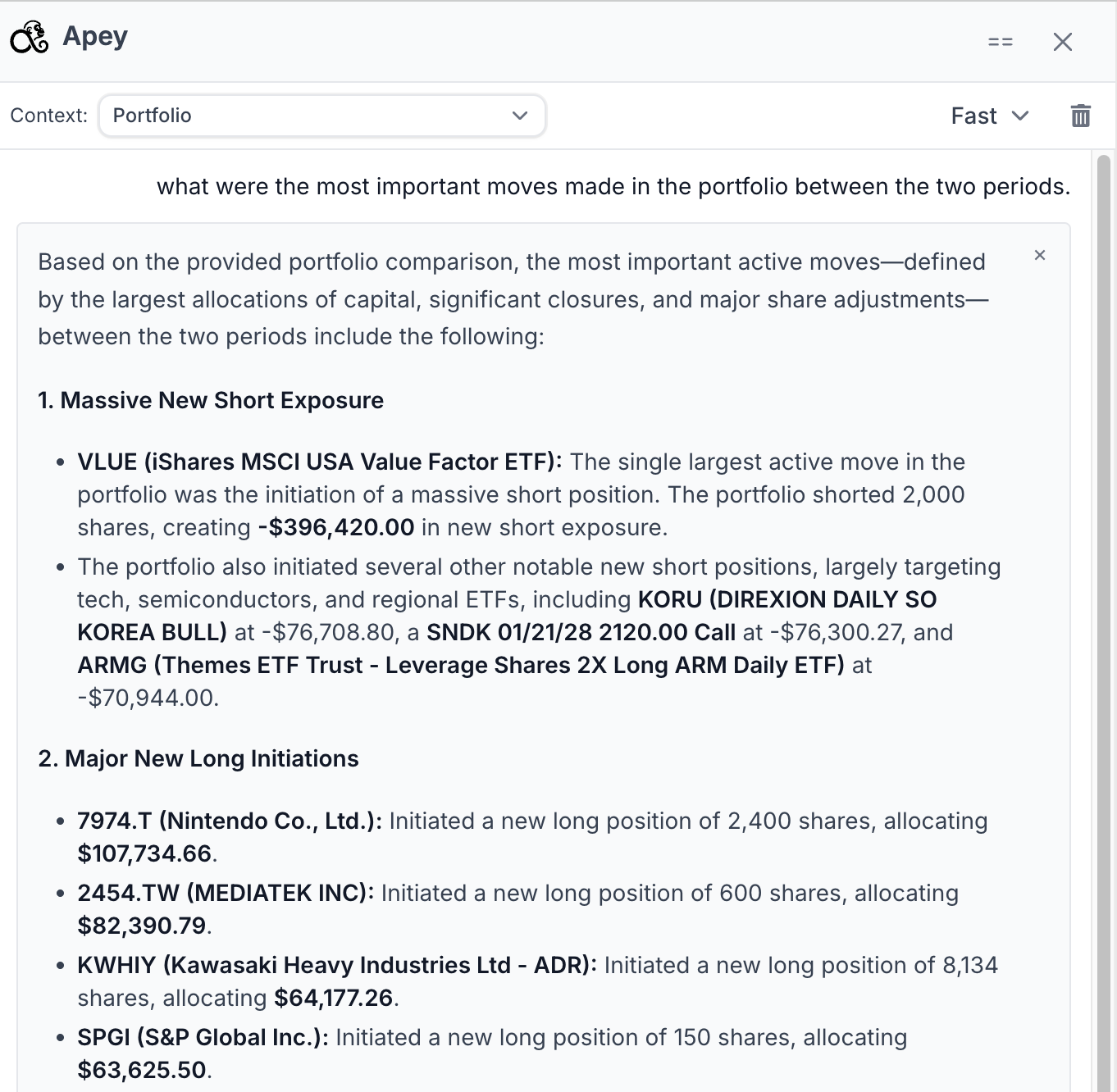

I got a quick recap of May’s decisions using Apey, the AlphaPort agent. AlphaPort is my investment research site. I won’t repeat his full output here, but actually this was pretty helpful if you want to try it out. Discord here if you want help getting setup: https://discord.gg/kABznx857

I won’t make you read everything Apey spit out (way more than the screenshot), but it does help me focus on the main moves. Lets go over each of them.

PSNL

Lets start with $PSNL, which Apey didn’t mention, as the position was opened right at the end of April. Last substack post, I concluded the post with some words about my desire to start diversifying away A LITTLE BIT from the AI/DC trade, aiming at a more balanced portfolio. This included taking on a position in $PSNL, which was trading around 2x cash, with significant volume growth (but limited monetization of that growth, as they figure out reimbursement).

I added a large position in PSNL, first at $5 a share, and then doubled down at $5.40. I have been wanting something in the biotech space for a while to diversify a bit. I really thought $NVO at $30 looked good but never really pulled the trigger (I did own a crumb for a hot minute but rotated it). $LLY also looked compelling going into earnings but I just didn’t think I could get good enough returns buying it here. Does look like that would have worked out too. That said, we are trying to multibag here.

Re $PSNL, I don’t know what my price target is here, but I have been following the minimally residual disease space for a long time (advanced cancer diagnostics) and like the space. At 2x cash w/ significant testing growth, I think PSNL is a solid business. Guidance for this year is around 48,000 tests, if you just slap a $2000 ASP on an MRD test, thats 96m = 5x rev w/ massive testing growth. Currently they are not hitting the $2000 ASP but we shall see.

This worked out very quickly. It turns out buying $PSNL for 2x cash was a good move, and the position is up 93.5k in a month, hitting $11.40 a share. I will hold it here. I also added a position in another cancer diagnostics company, $CAI which hasn’t run up as much yet. I’m going to make a Substack post fairly soon on the cancer diagnostics space. I find it very interesting.

$7974 / NINTENDO

I took a large position in Nintendo that is down small / is not working so far. I think i’m buying Nintendo at the bottom here as they are getting hit with increased DRAM prices.

This doesn’t sound like that big a deal, but management has suggested this will cost them about a billion dollars this year. On a 57b company that doesn’t sound that bad, but in terms of profit, it is about half of operating income.

In some ways, this is like buying an oil company when oil prices are at all time lows - I believe that the cyclicality will subside and I will be left with a great asset at a cheap price.

On top of the DRAM shortage, although the Switch 2 is selling extremely well, we are yet to see a major title announcement for it (maybe June 25 at Nintendo Direct).

So why buy?

Well, my view is that Nintendo is the Disney of our time and that they have finally found a hardware format in the Switch that has iphone like properties (eg they can just keep releasing new Switches indefinitely). Their transmedia moves are well thought out and cement a difficult to replicate brands importance, from their movies (which are doing extremely well in the box office) to their theme parks.

Is the company already too big to make a lot of money?

I’m not sure. We have gone from $24 a share to $11 a share in less than a year. As far as I can tell, outside of the DRAM issues, long term everything is fine. The switch is selling incredibly well, the IP is stronger than ever.

So, I am basically making a mean reversion trade here. I think once the memory crisis subsides (perhaps with CXMT flooding the market…) Nintendo will quickly regain some of its value, and I will probably exit at that point, maybe around $15-16 a share, so 50% in 18 months would be the idea, with somewhat limited downside risk in my view.

The dream way for the next 18 months to play out for me with the memory cycle is

SK Hynix lists its ADR in the US

SK Hynix then proceeds to make well over 200b in operating income in 2027.

SK Hynix has said that after increasing capex and building a 60b USD cash cushion, they will increase capital returns - there is at least 100b leftover here, so that would be an insanely huge special dividend or buyback.

SK Hynix goes up a lot.

I hit long term capital gains on SK Hynix.

I sell SK Hynix.

Another year passes, and although SK Hynix plays their hand well, an integral part of next-gen memory architectures (HBF etc), explosive growth seems difficult from here.

Although pricing on NAND/HBF/HBM maintains high prices, pricing on lower end DRAM drops. Nintendo COGS are reduced and earnings go back up.

I sell Nintendo +50%.

Rub all the moneys on my chest.

I am super long memory long term, but I do feel like we are moving to next generation memory architectures within a few years. I will make a substack post about this (Are you a memory_man part 2 coming this month).

That would be the dream way for the next 18 months to play out - but I also think there is a scenario where the Nintendo Direct coming in June is simply very good and a key title is announced, that leads to a quick 30-40% gain. Although my price target is higher, if I ‘realize my equity’ that quickly I will probably just take the W. Realizing your equity is a concept from Poker (i used to play for a living), and I think it applies to investing too. The basic idea is your hand has a lot of value, but it might be quite difficult to realize that value the way things play out (some chess scenarios are like this too).

The most similar concept in investing is “Having a catalyst”. So, there are really two catalysts here for Nintendo, a marquee title being released at Nintendo Direct that leads to some mean reversion (not the reason i’m buying, but a very clear upcoming event), or just normalization of pricing trends in 18 months or so for pure commodity DRAM (more reasonable in my view, but verrryy murky, and will probably involve plenty of Martin being bullied for being a bagholder).

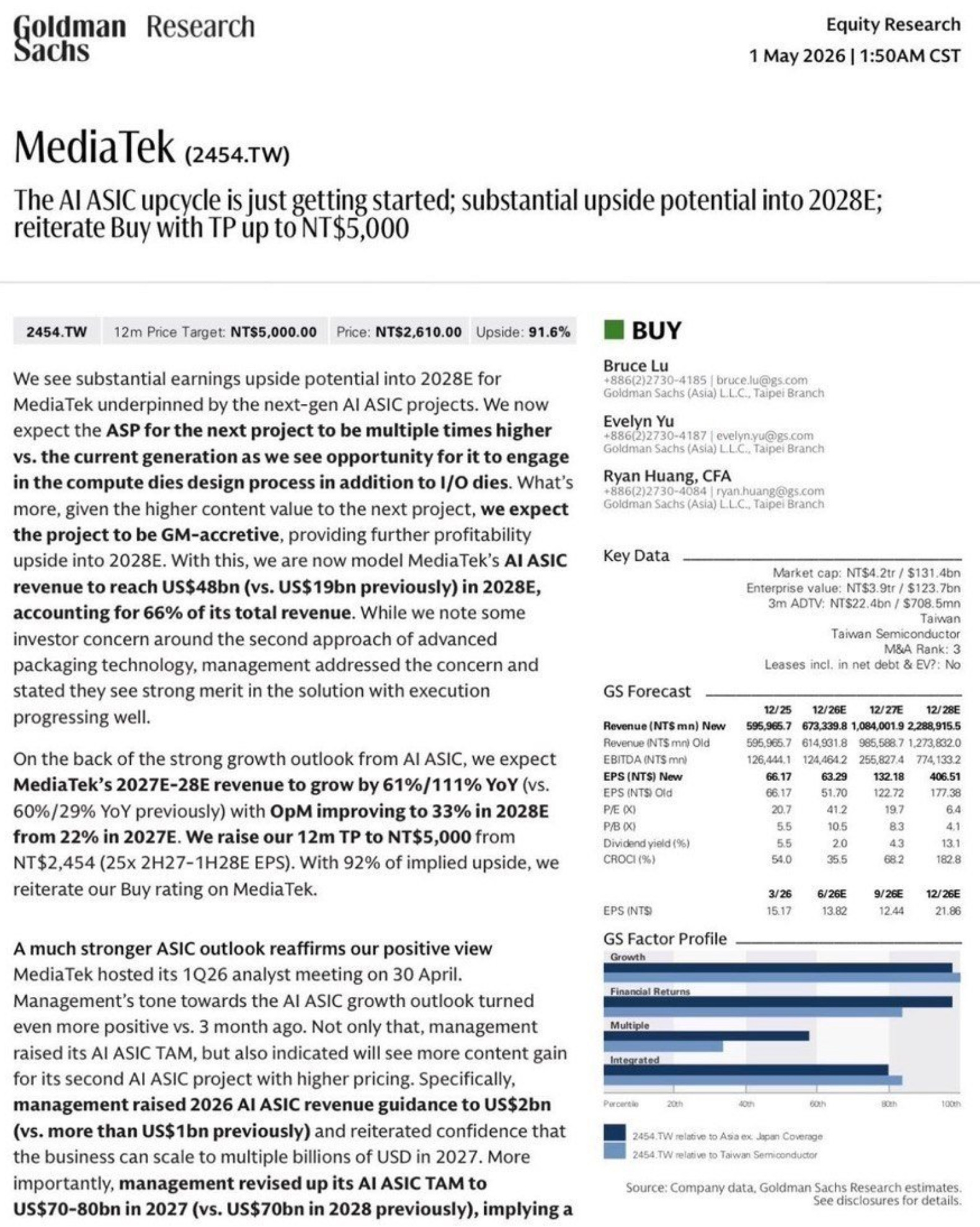

MEDIATEK

I can’t do better than Goldman Sach’s thesis on MediaTek right now so I am just going to post it in full. The basic situation is MediaTek is becoming an increasingly important player for Google. For TPU9, Google is splitting up the training TPUs and the inference TPUs. Broadcom is the design partner for TPU training going all the way through to 2031, but MediaTek is now taking on the job of TPUi, the inference TPU. Inference is pretty important.

So, MediaTek released a strong guide suggesting they will capture a significant portion of all next-gen ASIC TAM (10-15%). It’s worth listening to their last call if you’re interested in the spot.

Since then, more developments

Early May - MediaTek hires Douglas Yu, a former TSMC executive who spent years leading advanced packaging R&D

Late May - TSMC’s advanced CoWoS packaging capacity is currently stretched incredibly thin, largely because Nvidia is consuming so much of it.

Because Google needs to scale its inference TPUs to the millions, MediaTek and Google realized that relying solely on TSMC for packaging was a massive potential weak point. To solve this, MediaTek announced it is adopting Intel EMIB packaging alongside TSMC’s services (good for Intel longs…).

Thus, MediaTek finds itself as the key partner for Google

Major TSMC customer that can handle their manufacturing

Provide crucial IP on the chip itself (serdes)

Able to handle packaging between both Intel and TSMC.

Google has a goal of reducing its reliance on any one partner, and to some extent, this partially caps MediaTek’s upside. But MediaTek gives them the technical know how to reduce their reliance on both Broadcom and TSMC in one go. We have already rerated a little on this thesis, but at 220b market cap today, there is still room to go. Broadcoms market cap is 2.2 trillion. Broadcom does also include VMWare (bought for EV 77b), but if you cut that out, the value of their design business is significant.

Outside of TPUs, MediaTek also makes the Dimensity smartphone chip which is a premium brand and competes directly with Qualcomm Snapdragon in China, and they have an automotive chip business too. As Google Gemini penetrates every surface of reality, from the phone, to laptops, to the car, the data center, and eventually humanoid robots, its not hard to see how MediaTek is positioned to become the key partner, capable of operating at the cutting edge with both Intel and TSMC in literally all of these end markets.

Google is not the only one who realises this - Ming Chuo recently posted about MediaTek’s potential role as a design partner with for SpaceX’s Terrafab:

I find the arguments compelling, and even here, I don’t feel like I own enough. The only issue is it completely destroys margin on IB, and I can’t buy it in my LO account, so maintaining a large position is quite hard. Though I do not run net leverage, shorting stocks chews up your margin. I owned a little more earlier but trimmed slightly around 4600 to buy more unmarginable taiwanese stocks. Blech though it does look like so far that has worked out ok.

KWHIY

I took a position in Kawasaki Heavy Industries after looking at Mitsubishi Heavy for a while. The heavy names are completely undisruptable from AI and benefit. For example, Mitsubishi makes gas turbines, very in demand. Ships. Aerospace. Etc. Their backlog is about the same as total market cap.

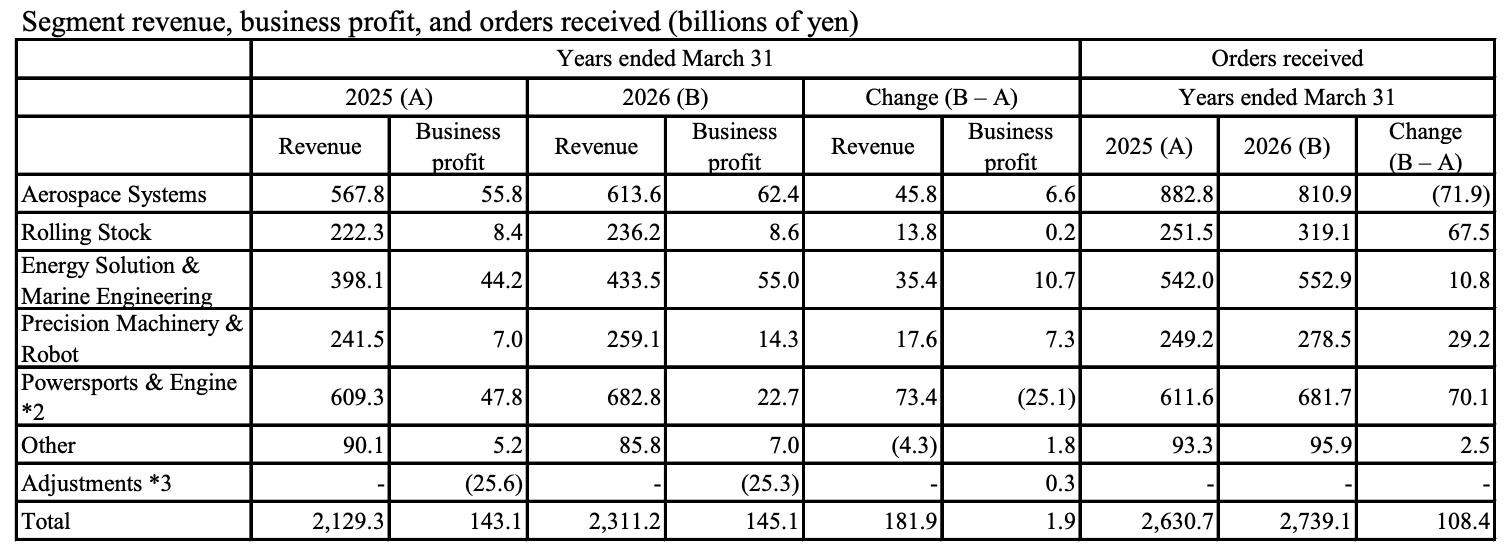

Kawasaki Heavy is similar. Here’s the revenue breakdown

KHI are guiding about a billion of profit in 2026 so paying about 15-16x, but they have solid growth and this is a pretty good price relative to market comps. The main markets we care a lot about are doing well. Aerospace, Precision machinery and Robot and Energy). PM&Robot is especially promising, with 17% rev growth and >100% operating income growth.

None of this is why I bought though. Nvidia recently said they are partnering with Kawasaki Heavy on robots, with a design center opening in San Jose (https://global.kawasaki.com/en/corp/newsroom/news/detail/?f=20260522_8524).

Jensen Huang made an announcement on youtube about it

“Together, Kawasaki and NVIDIA are building the foundation for a new generation of intelligent machines. You will use NVIDIA systems for AI training and simulation. With NVIDIA Omniverse and Isaac Lab, Kawasaki can connect simulation to reality. And NVIDIA Jetson would be the computer to run these” (this little video would be worth +1000% if KHI was a small cap shitco based in America fyi).

Jensen then goes on to point out the specific end markets: Medical Robots, Service Robots, Humanoid Robots and Mobility Systems. Kawasaki Heavy’s play in each end market has high upside optionality, especially Hinotori (surgery robot) and potentially Kaleido (humanoid robot).

At 15b market cap, if they are able to do anything in any of these spaces, you kind of have a pretty big free call option here. Market comps are much higher (look at where $BOT is trading..). This is a theme that’s been floated for a while now, the idea that previous industrial leaders will get rerated as they enter the humanoid robot space (Toyota may eventually do this).

The main issue I have after doing a little more research is the 9th generation Kaleido robot seems just kind of… like… it doesn’t look like it works that well vs the stuff we’re seeing out of Figure or Boston Dynamics.

Now, don’t get me wrong - Kawasaki Heavy’s main business is to service heavy industries. They make cargo doors for the Boeing 777. They’ve put stuff on the international space station. They make gas turbines, Helicopter engines. All kinds of stuff. So, I assume that when they make a humanoid robot and say they want it to do dangerous work, they understand a) the actual demands of the end market, and b) what the right form factor for that robot is. But to me, the Kaleido 9 robot looks a little like someones Gundam fantasy.

On the flipside, i guess if you are working on a construction site or oil rig, you need a helmet. You’re not just going to walk around with your nice Boston Dynamics Atlas style Lidar-Head.

The other thing that gives me pause is Kawasaki Robotics has quite the long term timeline.

“Around 2030, humanoid robots are expected to be used primarily in controlled environments such as factories and plants. In these settings, they will perform independent work under remote control and support people in their daily operations.”

K.H. is already selling Cobots into these end markets, so to me, this is very slow. Figure, Tesla and Boston Dynamics are doing this type of work TODAY. It is debatable the actual efficiency of the work, but it does mean that even though we’re on Gen9 humanoid robots, we’re probably at least 3 years behind.

K.H. goes on however.

“Looking ahead to around 2040, humanoid robots are expected to be capable of operating autonomously in unstructured environments while continuously recognizing and understanding their surroundings. Their applications are envisioned to expand into more complex and highly dynamic workplaces, including tasks performed at heights, in confined spaces, and at disaster response sites.”

Now, this is a clear vision I can get behind. Every day I walk past a construction site on my way to work, and probably half the time I sort of mentally imagine Optimus or Figure robots trying to work on the site. It seems HARD. But it doesn’t seem impossible. And having a really clear use case, rather than ‘does everything’ seems powerful to me. KHI wants to have robots that work in the same end markets they already service. Good. And honestly, 2040 seems realistic. For a humanoid robot in a controlled environment like a factory, shorter timelines make sense (look at Figure’s robot flipping packages). The home environment is much more complex and delivering a product that actually adds value is very hard, but people will be relatively accepting of failure in Gen1. Even just being able to talk to physical ChatGPT is already pretty wild.

But for a business to buy this product to work on a construction site the bar is pretty high. It needs to make the business money. 2040 seems realistic to me. But 2040 is also fucking AGES away. I want to potentially multibag in a year in this market. It might not happen, but if earnings inflect and the story plays out, I want to get paid straight away. That might seem greedy, but that’s the world we’re living in right now. If i am right about something, 2040 is too long to wait.

So, might have shot myself in the foot here - buying Kioxia was probably better even though the goal was to keep exposure to AI down a bit.

SPGI

That leads us to SPGI. I have been short FactSet for a while now (in and out, overall has gone well although not so much the most recent one), so why buy SPGI?

There’s a few reasons, but since this is long, i will try to be concise

1. I bought at $404 a share. Chris Hohn recently loaded up in Q1, his best possible cost basis is $390. C.H. is one of the few GOATs i really rate highly (along with Druck, Tepper and Weschler). He sold a bunch of stuff to buy SPGI, so, had to pay a lot of tax. So I think I am roughly getting his entry here, maybe even better. That’s a great starting point.

2. Wanted to diversify a little away from AI.

3. The Platt’s energy data business has done very well lately, and I have no idea how to get their data. I know how to generate all of FactSet’s data. No idea how to get this stuff. That makes it pretty valuable.

4. S&P business is amazing.

5. Bond rating business is doing well with AI buildout (as companies want to issue debt to build out AI data centers, they need ratings on that debt).

6. S&P business is amazing.

Since this is long, i am just going to go into one or two details on Part 4/6.

How does SPGI make money?

Well, the crown jewel of their business is licensing off the S&P index. For example, they maintain the list of 500 companies that go in $SPY. That might sound simple, but simple or not, competing with SPY is very hard.

Why?

Well, some portion of market participants prefer to buy SPY as their selection of companies of choice. Once those participants start buying, the index starts to amass liquidity which leads to tighter spreads. This becomes a self reinforcing cycle, where investors accrue large amounts of capital gains (making it difficult to sell), the AUM of the index goes up, liquidity increases, and the cycle reinforces itself.

VOO is extremely trusted (you probably own some). SPY too. Did you know that of the .09% expense ratio, SPGI makes .03%?

So if SPY has AUM of $783 billion, State Street gets a MER payment of $704m. But they have to pay .03% to $SPGI for licensing the S&P 500 brand.

There is really no way out of this. SPY has liquidity. If my mum wants to buy an index fund, i’m going to tell her to buy VOO or SPY, because they have low fees and because the spread is tight. So, you basically have a bond, but…

the bond grows at the rate of an equity (as the companies in the index go up in value, AUM is higher, so we rake more)

The bond also grows at the rate people invest more in ETFs (huge portions of boomer wealth are still rotating into stocks from real estate and mutual funds)

The S&P licensing business is basically the best security in the history of the world.

SPGI also rakes VOO. My understanding is they get slightly less there, but the figure is not known. Whatever the case, the basic dynamic is the same - Vanguard cannot just stop the growth of VOO - in order to compete with it, they would need to have a similar index they managed themselves, but whatever that index was, it would have to have the same amount of liquidity or spreads would be very high. Want to push people to another security besides VOO? Your customers might just move to SPY. And so, the cycle continues. This is one major reason Hohn likes SPGI (the other being that the bond rating agency has similar characteristics - the trusted brand rating the bond lets the company issue the bond at a lower interest rate, and the cycle perpetuates).

Ok, that’s enough on specific names.

Exposure

I will take a moment here to mention a couple newish features i’m using with ALPHAPORTT.AI to make handling my exposure more accurate - you might have noticed earlier that in the screenshot, I have -17k of cash. and yet my net exposure is 85% (my general target at all times). This is because the site has multipliers on positions like $KORU. So a $76k KORU short is actually more like a $220k short (short -110k of Korean Memory against the Hynix long).

This is actually pretty useful if you run a portfolio like mine - your exposure can easily get away from you.

I’ve actually added another feature recently that lets you break your portfolio into different segments. This helps gauge how much exposure I have to the AI trade. For example, KORU has a 3x multiplier, but I also mark it as ‘50% AI’ (half the index is just SK Hynix and Samsung, although they do sell into non-data center markets most the earnings growth is from AI).

With these modifiers, I can see my true net exposure to the AI trade. I am long 1m of AI stocks, and short 600k, so of 1.54m total, we are at about 24% long AI. Note that I am not including Google in this. When I say AI, I really mean ‘the AI buildout’. In a world where capex levels off, I actually believe Google is extremely well positioned. That’s the advantage of segments - this might be a weird way to think about it, but i’m a weird guy. You probably are too. Set up the segments however you want.

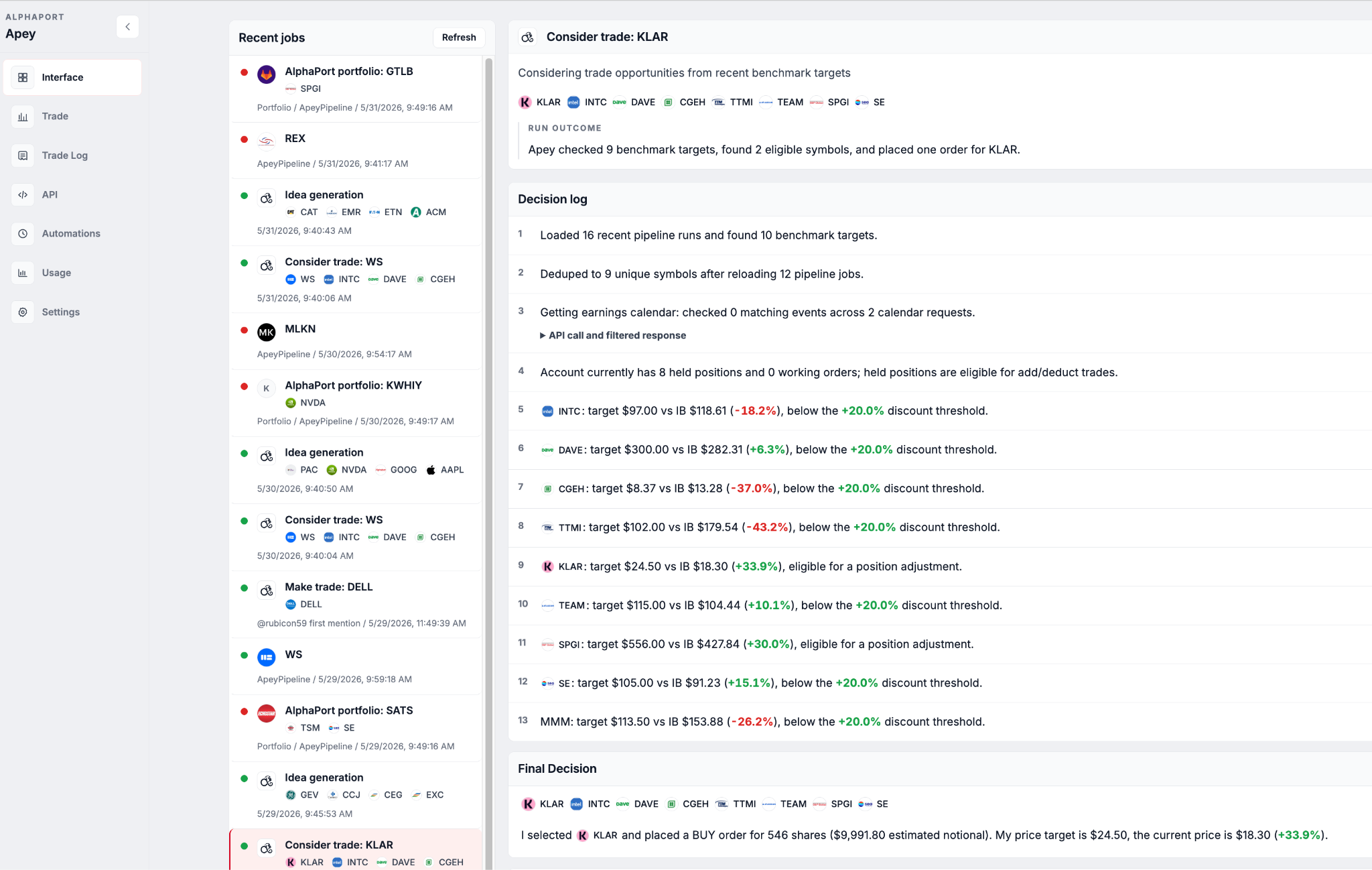

Using Apey to Trade Automatically on IB

On top of these new ALPHAPORT features, I am also running a parallel portfolio now, having an agent trade using AI Pipelines on the site. I will go into some more details on this in the future, but it is going pretty well so far.

It started with analysis on my existing positions, but it has now moved into picking 3 random positions from $IWM every day to do deep analysis. It then adds those to its database, and picks the best of all available positions each day. It then purchases them using the IB API, so its all completely automated at this point. Right now, it seems to LOVE Klarna (bought it 3 days in a row lol).

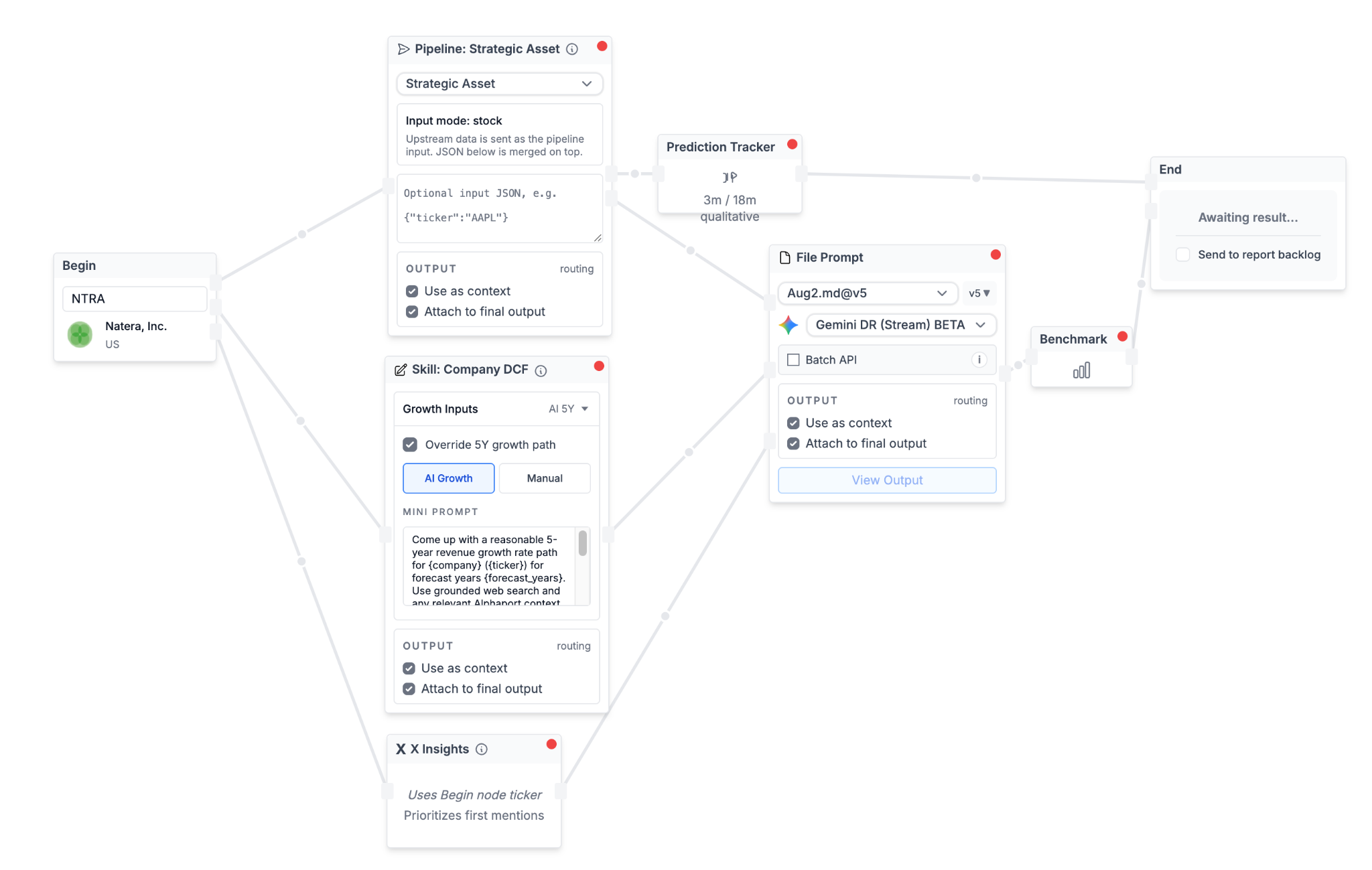

Currently I am keeping my pipelines fairly light as I ramp up the product. I build them using the ALPHAPORT visual builder, which lets you create multistep LLM pipelines and call them over API. ALPHAPORT lets you build nested pipelines as well, so the sky is truely the limit (eg your pipelines can call other pipelines).

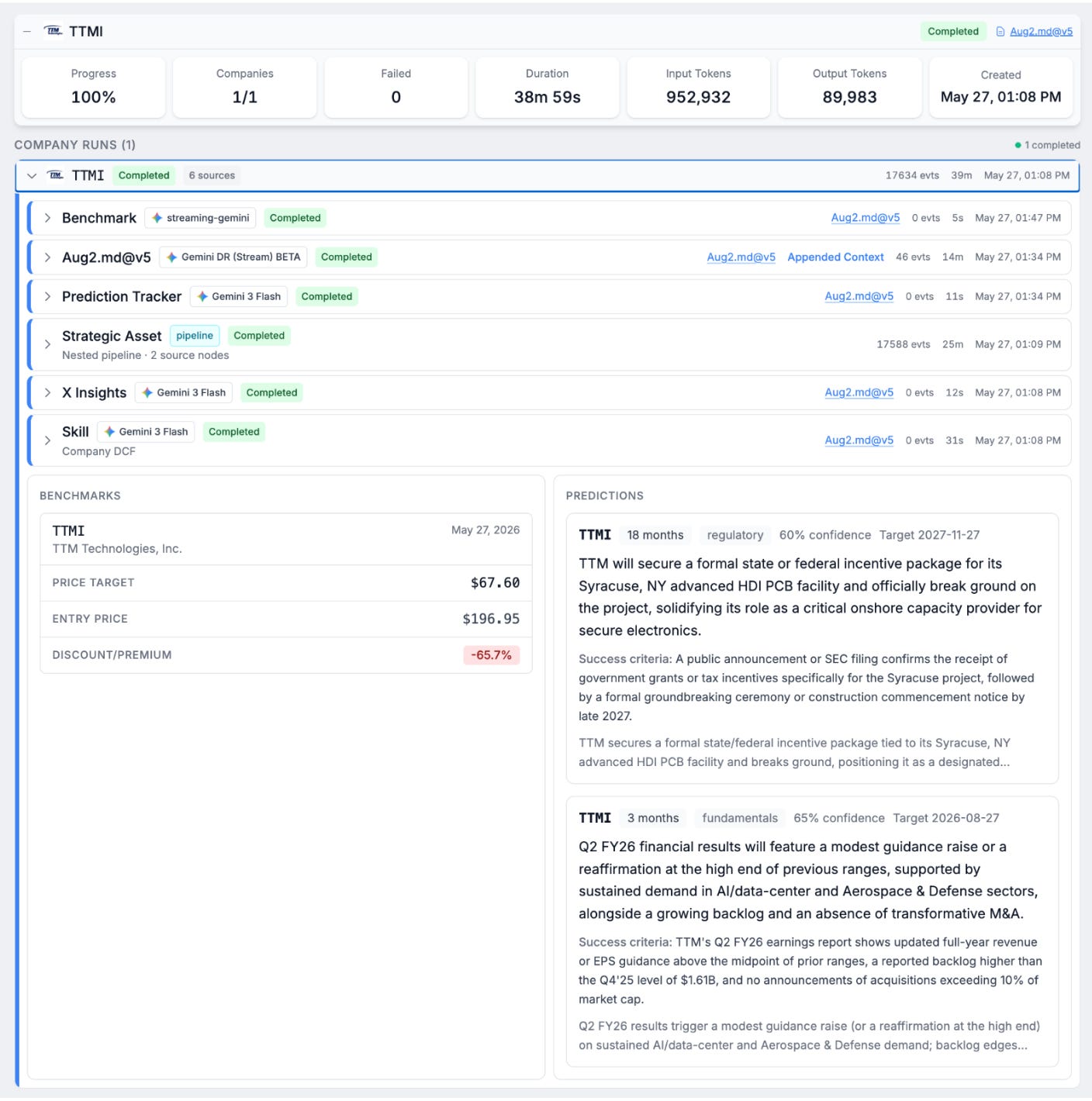

I expect this parallel portfolio to continue ramping up as I handle increasingly large amounts of coverage (EG all of IWM) and fine tune the agents decision making process. ALPHAPORT also gives you a nice pipeline explorer called SONAR, that lets you see the output of each step.

If that sounds like something you’d like to get more deeply involved in using, feel free to email me at martin@alphaport.ai, and I can do a video demo for you. The business model is to charge a modest % on top of the token cost (5-10%). Since a lot of basic stuff can be done without even hitting the LLM (eg screening for stocks that fit basic financial criteria before doing any LLM stuff), I actually think ALPHAPORT will get you both better results, AND cheaper requests, vs doing it yourself over API.

On top of that, ALPHAPORT gives you a beautiful way to view and share your portfolio. For example, here is my current automated portfolio, updated daily: https://app.alphaport.ai/shares/b0bfdd12-8dbe-456a-bf18-a874e53cace3

Although the portfolio looks pretty overweight Klarna, keep in mind that it is only 11% net long right now, as it slowly enters positions and I work out kinks etc.

Overall, its been a nice month executing on my 3 main goals

We had some modest substack growth

We finally getting this full loop to work, from the generative pipelines all the way to trade execution.

Crushing SPY despite not doing anything too insane.

Good luck in June.